The intention is to address topics and areas that we see gaps and malfunctions in the market and create hassle, cost and pain to the organizations.

We hope to provide food for thought that would trigger internal discussions on what and how could be improved

The Evolving Interface Between Biotech Companies and CDMOs

Biotechs are at the forefront of pharmaceutical innovation, driving new therapeutic approaches ranging from monoclonal antibodies to mRNA, cell, and gene therapies. But bringing these breakthroughs from lab bench to patients is an intricate journey that often depends on robust, strategic partnerships with CDMOs.

The collaboration between CDMOs and Biotech companies differs from that with traditional pharmaceutical companies (mainly marketing small molecules), reflecting each partner’s structure, needs, and development stage. Biotechs typically engage CDMOs early, often from lead optimization or preclinical phases, seeking scientific guidance, formulation support, and regulatory preparation. These partnerships are agile, informal, and heavily reliant on CDMO’s technical expertise, as Biotechs often lack internal CMC resources. CDMOs act as strategic partners, filling data gaps and accelerating timelines toward first-in-human trials. In contrast, traditional pharma companies tend to engage CDMOs for capacity expansion, specialized technologies, or cost-effective commercial supply. Their projects are usually better characterized, governed through formal processes, and supported by in-house CMC expertise. While Biotech-CDMO collaborations are defined by scientific innovation and flexibility, traditional pharma-CDMO partnerships emphasize operational rigor and long-term scalability. As CDMOs evolve, they offer integrated early-development platforms for biotech clients adapting their governance, capabilities, and culture accordingly.

Understanding how to build and maintain an effective interface between biotech companies and CDMOs is vital for accelerating timelines, ensuring product quality, and enabling long-term commercial success.

Early-Stage Collaboration: R&D and Process Development

Biotech innovations typically emerge from a research-driven mindset focused on mechanism of action, proof of concept, and early clinical results. CDMOs support in high-throughput screening, molecular biology, cell line and vector development, in vitro and in vivo studies. Additionally, CDMOs bring a different but complementary focus: robust process engineering capabilities, scalability, quality systems, technology platforms, and regulatory compliance that enable efficient scale-up.

For a successful and mutually beneficial partnership, alignment begins during the early development phase. Even before a clinical candidate is selected, discussions about manufacturability, formulation feasibility, and process development should be underway. This collaboration ensures that development strategies anticipate regulatory expectations, potential scale-up constraints and reduce the risk of costly redevelopment further down the line.

Clinical Trial Manufacturing: The Critical Middle Ground

The manufacturing of clinical trial material is a pivotal but often underestimated phase in the biotech product lifecycle. CDMO’s role shifts from technical collaborator to operational executor, managing GMP production, labeling, packaging, and sometimes even clinical supply distribution.

Clinical trial manufacturing introduces several layers of complexity:

- Production must occur under strict timelines tied to trial start dates.

- Yields may be low and processes still under optimization.

- Regulatory documentation must be developed in parallel with ongoing studies.

For early-stage biotech companies, delays at this stage can be existential. A well-integrated CDMO mitigates this risk by offering flexible capacity, small-scale GMP suites, and adaptive planning tools.

Tech Transfer: Turning Science into Process

Tech transfer is a multifaceted process that translates lab-scale protocols into industrial production, whether for clinical or commercial use. For biologics and advanced modalities, this often involves transferring not just methods but knowledge: rationale behind process conditions, critical quality attributes, and material behavior.

Challenges frequently arise from incomplete documentation, different equipment footprints, or unaligned analytical methods. These risks can be mitigated by:

- Engaging in structured tech transfer planning

- Assigning cross-functional leads from both sides

- Using a defined acceptance criteria checklist

Tech transfer success depends on clarity, consistency, and collaboration not only between teams but also between technical philosophies.

Supply Chain Integration: Beyond Manufacturing

A common misconception is that CDMO collaboration ends with batch production. In reality, supply chain integration is equally essential, especially for biotech companies developing global clinical or commercial programs.

Key supply chain concerns at the biotech-CDMO interface include:

- Lead times and raw material security

- Cold chain and temperature-controlled logistics

- Forecasting accuracy and capacity alignment

- Inventory management and regulatory labeling

Miscommunication in these areas can lead to stockouts, compliance issues, or financial penalties. To prevent such issues, successful partnerships build integrated planning cycles that include demand review, scenario planning, and real-time visibility dashboards.

Regulatory Interface: Coordinated Compliance

Regulatory approval is the culmination of years of development but it also requires meticulous preparation. CDMOs are deeply involved in the preparation of Chemistry, Manufacturing, and Controls (CMC) sections of regulatory filings, as well as in responding to agency queries.

A strong interface must cover:

- Early alignment on regulatory expectations (e.g., ICH guidelines, FDA/EMA requirements)

- Coordination of documentation timelines

- Clarity on roles for GMP inspections and audits

- Unified narratives for product comparability and process changes

Regulatory misalignment can cause months of delay. Early-stage planning and open communication throughout development mitigate these risks significantly.

Building the Right Interface Model

The Biotech-CDMO collaboration model is shifting from a transactional approach (outsourcing execution while retaining all strategy) to co-development of products and investing in strategic partnerships with shared risk.

Successful Biotech-CDMO interface typically shares three characteristics:

- Cross-Functional Engagement: Involving QA, Regulatory, Project Management, and Supply Chain—not just R&D.

- Governance Structure: Regular joint steering committees, issue escalation paths, and KPIs.

- Cultural Fit: Shared values around transparency, accountability, and problem-solving.

The Future of CDMO-Biotech Collaboration

Looking ahead, the lines between Biotechs and CDMOs will continue to blur. We would see more co-development models, risk-sharing agreements, and even equity-based partnerships. Digital transformation—through data integration, advanced analytics, and AI-driven process optimization—will further enable real-time collaboration and innovation.

Ultimately, the ongoing evolution of Biotech-CDMO partnerships is reshaping the pharmaceutical industry for the better. By combining scientific ingenuity with operational excellence, these collaborations promise to deliver new therapies to patients more efficiently and reliably than ever before.

Conclusion

As biotech products grow in complexity, so must the partnerships that support them. CDMOs are no longer just service providers—they are co-navigators in the journey from innovation to commercialization. Strengthening the interface across technical, operational, and regulatory areas is essential for ensuring that breakthrough therapies reach the patients who need them, faster and more reliably.

For both Biotech companies and CDMOs, the future lies in collaboration—not as a reactive necessity, but as a proactive strategic asset.

The Mystery Behind Pricing: Why Two CMOs with Same Direct Costs Quote so different Prices

Surprise, Confusion, Frustration and maybe also a wry smile can be the outcome of comparing commercial offers for the same product, coming from different CMOs. Pharmaceutical companies looking to outsource their products usually run an RFQ containing a handful of CMOs, asking the latter to provide their offer for a specific product (or a basket of products).

It is not uncommon that the offers received have a big difference between them, when it comes to the unit price. And this creates puzzlement or even uncertainty to the pharma company comparing them. The usual excuses trying to explain the big range, can be that the batch size and the manufacturing location are different, or that different API suppliers have been used, or maybe different packaging material specifications have been assumed.

But what if all the above are the same and also Direct cost is the same between different CMOs? But still, the difference in the price is big? What on earth is going on? How two CMOs with the same Direct Cost can provide so different unit prices for the same product? So, why even if batch size, location, API suppliers and packaging specs are the same between two CMOs, their prices have so big gap between them? And if we assume that on top of those similarities, the two CMOs have the Direct Cost, this is certainly a reason to go nuts… Or maybe Not?

Let’s, dig beneath the surface a little bit. As I like to say, first things first. Price is different than Cost and although sometimes they are related, it happens very often that they are not. So, when the effort to explain the difference in prices between CMOs starts from the cost, this can lead to wrong expectations. There are more things that might explain the mystery, and in this article, we will try to shed some light on it. In doing so, we will use an example comparing two CMOs with the same Direct Cost asked to quote for the same product to the same customer.

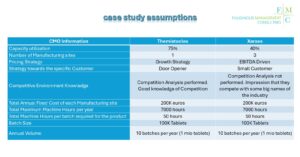

Let’s call the first CMO “Themistocles” and the second CMO “Xerxes”. And below is some information about them but also for the requirements of the product:

Assuming that both of them were asked by the same customer to provide an offer for the same product, the first thing they do is to calculate their direct cost. And then their fixed costs and overheads before deciding what price to offer.

Starting with Themistocles.

Direct cost for the product is already calculated and is assumed to be 15 euros per 1000’s tablets.

So, on top of it, fixed cost, overheads and margin should be added in order to calculate a price.

Fixed Cost Hourly Rate: Total Annual Fixed Costs / Total Annual Machine Hours x Capacity Utilization

So, for Themistocles this gives a fixed cost hourly rate of 38.1 Euros per Hour {200K / (7000* 75%)}. Considering a batch size of 100K tablets and that 50 machine hours per batch are required, the fixed cost is 19.05 per 1000 tablets. {38.1 x 50 hrs / 100K tablets)

Since Themistocles operates 1 manufacturing site, there are no corporate overheads to be allocated to the site. These costs usually have to do with corporate functions like corporate Finance, corporate Quality or corporate business Development and are common expenses serving as support functions for different manufacturing sites. Overhead Costs: 0 per 1000 tablets.

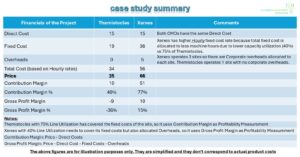

The business Case for Themistocles is as follows:

Direct Cost: 15

Fixed Cost: 19.05

Overheads: 0

Total Cost: 34.1

Since cost has been defined, now its time for adding a margin. Remember that Themistocles has 75% utilization rate meaning that probably fixed costs have already been absorbed from existing products on the site. 10 batches per year for the specific product, most probably will not require additional fixed costs (like a new Site Director, or New Supply chain Manager, additional rental, or additional utilities like heating for offices).

Therefore, Themistocles uses “Contribution Margin” to calculate its profitability. Contribution Margin is Price minus Direct Costs. Fixed costs and overheads are not considered in this profitability measurement. For as long as, the fixed costs do not go up if new products enter the site, contribution is the real profitability and what it goes directly to the bottom line of the site.

So, keeping in mind that the specific customer will work also as a door opener and Themistocles has a growth strategy, he is happy with a contribution margin at 40%. This will give a price of 25 euros per 1000 tablets and contribution margin of 10 euros per 1000 tablets. This price covers all direct cost and although (according to the hourly rates) does not cover fixed costs, this is not relevant for Themistocles since these costs have been already covered. In annual terms this project will result in 25K euros and 10K euros profitability. So the spent for the customer will be 25K euros if he selects Themistocles.

Lets do the calculations for Xerxes now.

Direct cost for the product is already calculated and is assumed to be 15 euros per 1000’s tablets.

So, on top of it, fixed cost, overheads and margin should be added in order to calculate a price.

Fixed Cost Hourly Rate: Total Annual Fixed Costs / Total Annual Machine Hours x Capacity Utilization

So, for Xerxes this gives a fixed cost hourly rate of 71.4 Euros per Hour {200K / (7000* 40%)}. Considering a batch size of 100K tablets and that 50 machine hours per batch are required, the fixed cost is 35.7 per 1000 tablets. {71.4 x 50 hrs / 100K tablets)

Remember that Xerxes operates 3 manufacturing sites and there are corporate overheads that need to be allocated in the sites. Let’s assume that the after doing the calculations, for the specific project the overhead cost per 1000 tablets is 5 euros.

The business Case for Xerxes is as follows:

Direct Cost: 15

Fixed Cost: 35.7

Overheads: 5

Remember that Xerxes has a low utilization rate and fixed costs have not yet been absorbed by the existing products. Moreover, the EBITDA related strategy means that every project should have a minimum profitability that should cover all costs and also leave a margin. This means that Xerxes cannot use contribution margin as a profitability measurement. Instead, he should use gross profit margin measurement. This measurement considers that all costs need to be removed from the price to determine what profitability the project will leave.

Moreover, this is a customer that for Xerxes is not considered important, meaning that he is not ready to sacrifice his profitability.

So, even with a gross profit of 15%, Xerxes would have to give a price of 65.75 per 1000 tablets and gross margin 9.86 per 1000 tablets. This price covers all direct and fixed costs and overheads and leaves some profitability on top. In annual terms this project will result in 65.7K euros and 9.9K euros profitability. So the spent for the customer will be 65.7K euros if he selects Xerxes.

This is a difference between the two CMOs of 40.75 per 1000 tablets or putting it in another way, Xerxes price is 2.6 times higher than Themistocles.

This might look like an extreme example but the truth is that experience has shown that such differences can occur in real life. In Fuliginous Management Consulting we have run RFQs on behalf of our customers where the lowest from the highest price coming from different CMOs can be 3 times away or even bigger.

And this is the top of the iceberg since we have not taken into account factors like batch size, machine output, manufacturing location which impacts direct labour cost, not even how different CMOs approach material costs. There are some CMOs for example who just add a small % on top of their material costs (to cover the working capital for example) while other CMOs apply the same profitability % as the one they use for the overall product. So if the latter want to have 15% gross profit, then they will apply this also on materials. If the materials is a big part of the price, then the difference with other CMOs can be significant.

And of course, this proves that a big number of CMOs do not spend time on understanding what the customer is willing to pay for the specific product. Putting yourself in the shoes of the customer is something that takes time but at the end of the day it improves the probability of success in RFQs.

Cost Plus Pricing Model alone is introvert and does not take into consideration the market peculiarities. Market Minus model (what the customer is willing to pay) and Benchmark of the competition (what other CMOs offer on average for similar technology products) should be in place if CMOs want to win as many RFQs as possible that are relevant to their strategy.

So next time you receive offers from different CMOs with a big range, there is no need for surprise, confusion or frustration. Its not that expensive CMOs want to “steal” you, they just have different pricing strategy, or they have not gone deep enough in their costing and profitability policies. It might be also the case that the CFO and the Commercial Director of the CMO have different views on how the ideal project looks like. And it might be also matter of timing. At different time points the same CMO may have different utilization rate, different equipment, or different profitability targets.

Trying to solve the mystery behind pricing requires deep knowledge of the pharma CMO industry, costing and pricing. But one thing is certain. By understanding factors that influence CMO pricing, Pharma companies can make more informed decisions and avoid unnecessary confusion or frustration when comparing offers.

European CDMOs offering. Looking for a needle in a haystack. It shouldn’t be…

Hi George, I have a quick question for you: “do you know what level of CDMO capability exists within Europe for Ampoules and PFS manufacture of hormonal products?”

This was the question I received from one of our partners some time ago, worried that the options might be limited in this area, and she would struggle to identify a suitable CDMO in case a change of source would be required in the future.

I don’t think that my reply was very reassuring since there are not so many European CDMOs that are able to manufacture high potent steriles. There are around 30 of them mentioning that they can offer this kind of technology, but if you look deeper, you will see that most of them can fill glass vials only. For amps and PFS the number should be around 10-20. And if you look even deeper, you will see that most of them can go up to OEB 4. So, depending on the toxicity level, the annual volumes required, and the timelines for a tech transfer for such a product, options can be indeed limited. Let alone pricing.

Therefore, my reply was that it will not be a walk in the park to identify a CDMO for this, but for sure finally someone will be able to do it.

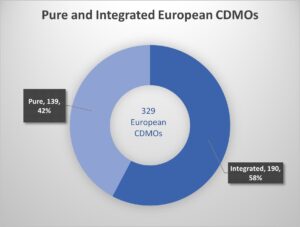

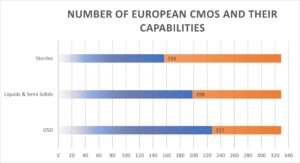

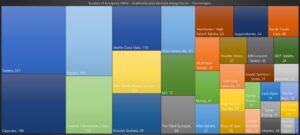

There are around 330 European CDMOs offering commercial batches of finished dosage forms and they operate around 540 manufacturing sites in the continent. Some of them are pure CDMOs and some are what we call integrated ones. The difference is that integrated CDMOs market their own products while pure offer only contract development and manufacturing services to their customers without a product portfolio of their own.

According to our research, 42% are pure and 58% integrated CDMOs.

It does not come as a surprise I think that most of CDMOs can offer OSD forms like tablets and capsules. Of course, within OSD there are more technologies other than tablets and capsules and if someone is looking for a CDMO able to produce pellets for example then they should have to restrict their search a lot. The options get even more limited if someone is looking for niche OSD technologies like spray drying or hot melt extrusion. So, although in total there are 227 European CDMOs offering OSD forms, just a small portion of them can offer technologies that separate the best from the rest.

And the same more or less goes for Steriles. Although there are 156 European CDMOs offering sterile products like amps and vials, if someone is looking for sterile bags then immediately their options go down to 18! Let alone if a combination of parameters is needed like high potent steriles filled in bags. Then this is 1 figure number…

This kind of information is important in my eyes not only to pharma companies looking for suppliers but also for CDMOs that they want to understand their competition. There are many external manufacturing departments in different organisations that don’t have the time to spend in analysing the CDMO market. And there are very few CDMOs that spend time in understanding the competitive environment in which they operate. In both cases, this lack of understanding can result in missed opportunities. Pharma Companies with big product portfolios, end up with huge complexity in terms of the number of suppliers they work with and CDMOs don’t know what kind of competition their offering faces. And this can have an impact on their pricing decisions resulting either in loosing business or leaving value on the table.

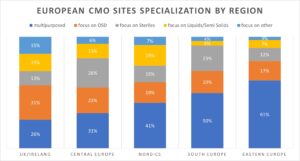

Another area that is interesting to shed some light on, is this of specialization. In which technologies (if any) different manufacturing sites in Europe focus on. Are the majority of sites focus on 1 technology or they are what we call multipurposed? This can be considered important in some cases, and it has to do with the type of products a pharma company has in its portfolio. A generic pharma company with various product types, may find as a strong point if its suppliers (CDMOs) have multipurposed sites, since they will be able to allocate to such sites various products of different technologies, reducing as a result complexity in their supply chain.

On the other hand, a pharma company offering only sterile injectables to their customers, may find it reassuring that their suppliers (CDMOs) have manufacturing sites focusing only on such products. This might be because a high degree of expertise as well as higher cost efficiency can be expected from such sites on the specific technology.

External manufacturing network departments of different pharma companies may be happy to know that there is enough of both types of CDMOs. 56% of CDMOs specialize in 1 technology and 44% can offer more than one.

The question is those CDMOs who focus on something, where they focus on? the answer is that the majority focus on OSD (18%), and then Steriles (14%) and Liquids/semi solids (10%) follow. But here there is a catch!

If we take a closer look and we take into consideration the European region where different sites operate, we will see that different regions have different patterns when it comes to specialization. Multipurposed sites are much more common in South and Eastern Europe compared to Central Europe and UK/Ireland. So, if a pharma company is looking for a CDMO with multipurposed facilities in UK or Germany, it will have a much harder time to identify one compared to someone looking in Poland or Greece for example.

There must be a reason behind this discrepancy between European regions when it comes to specialization, but we can analyze this in future articles.

For the moment, lets keep in mind that there are many CDMOs in Europe, some of them big, some of them mid-size but most of them small and relatively unknown. But they are unknown because very few external manufacturing departments spend time to get to know their suppliers and their capabilities, let alone build a strategy behind their external manufacturing network optimization. And this is a pity because without a proper strategy in this area, managing external partners becomes more and more expensive.

And while CFOs and Supply chains will argue forever how a preferred supplier looks like, it is for the best of the company to get to know the CDMO market and then decide how to build its strategy.

After all identifying the right CDMO should not be like looking for a needle in a haystack…

Opening the door to new customers in the CDMO industry

“Sorry George, but we will not participate, we are a small CDMO and we have too many running projects at the moment”. This was a reply from the CEO of a small CDMO when I asked him if they would be interested in participating in one event, where Fuliginous Management Consulting has been invited to talk about CDMO landscape Trends and Pharma Co’s Outsourcing Patterns.

At the same time, we received positive feedback from other CDMOs that are somewhat a bit bigger or medium sized. And then I started thinking how a small CDMO located in central Europe is full of projects and they don’t have the interest in participating in an event which would also give them the opportunity to make several one-to-one meetings with prospects.

And then I started looking at the capabilities of this small CDMO and compare it with the capabilities of the midsize CDMOs. There must be something that this small CDMO does very well and maybe its competitors don’t do it. Fuliginous Management Consulting’s capability mapping for finished dosage forms for small molecules is so complete that it was easy for me to compare the manufacturing capabilities of different CDMOs.

So, I refreshed my memory about European CDMOs and their capabilities. Nobody forgets the big names of the industry that usually offer a big range of products such as solids, steriles, liquids, creams etc. But there are also small CDMOs out there that seem to be successful and kept busy. What can differentiate a small CDMO from the 330 others that operate in Europe and also offer CDMO services? Located in central Europe, costs cannot be much lower compared to competition. Customer focus might be higher than some bigger CMOs, but again it cannot explain how busy this CDMO is. Pricing (which is different than cost) might play a role in success but then again, pricing has to do with so many parameters (or at least should do so) that alone cannot guarantee success. Other factors like quality, delivery performance etc. are of course important but again, something else should make the difference. Good quality and delivery performance do not open the door to new prospects. They are important to keep customers in, but something else needs to bring them in first. And the same more or less goes for competitive pricing. It is important to open the door to a new customer, but first the new customer should knock at the door.

So, what makes a customer knock at the door and ask a CDMO if they have the capability to quote for a specific product? Being in this industry for almost 20 years, out of which the last 5 of them spent in understanding the CDMO market, my opinion is that small CDMOs can survive in this competitive landscape if they do something different and something better than the masses.

So, “Specialization” is the word I was looking for.

Many (almost 70%) of small molecules European CDMOs for finished dosage forms can produce OSD (Oral Solid Dosage) forms. And around 50% can produce Sterile products. But how many of those producing OSD can produce high potent OSD and how many of them can offer hot melt extrusion or spray drying? And from those producing steriles, how many have the capability of producing high potent steriles and sterile bags or PFS?

The answer to the above is that less than 20% of European CDMOs produce PFS, less than 7% offer high potent steriles and only around 5% can fill sterile bags. And the same goes for spray drying and hot melt extrusion. Around 5% of European CDMOs have these capabilities. If someone is looking for capacity in PFS, they will have a bigger choice since around 20% of European CDMOs can now offer them.

But what was this % some years ago? Not only for PFS but also for all the above-mentioned technologies? I cannot say for sure but definitely 10 years ago, you could not find so many CDMOs offering high potent OSD and prefilled syringes. The reason for this increase and the evolving number of CDMOs offering new technologies is of course the demand for such technologies.

Taking a look at the new drug approvals from the FDA during the last 5 years it is clear that there is a trend. New products entering the market are high potent, steriles, OSD difficult to be manufactured due to poor API solubility, lyophilized etc. Moreover, within sterile category, prefilled syringes % grows year after year. More specifically, new drug approvals in PFS accounted for 30% of sterile product FDA approvals in 2023 while in 2022 and 2021 the figure was 20% and before 2020 even lower. And the opposite goes for other technologies that used to prevail some years ago, but not anymore.

This means that CDMOs that understand the market trends and follow the demand, before competition, have a competitive advantage. CDMOs that specialize in certain technologies and are very good at it due to expertise, also have an advantage compared to competition.

Spending time and resources to build the right CDMO strategy for the future, certainly is something that will pay off eventually. Where to invest, what to expect from this investment in terms of revenue and profitability and what customers to contact, is something that is a requirement in today’s environment. Deciding to specialize in ampoules as opposed to PFS or lyophilized vials for example has some implications. Different technologies have different demand, require different pricing and bring different profitability. The profitability % that a CDMO should expect from producing conventional tablets should be less than this of lyophilized vials for example. And the opposite goes for the annual volume. Probably annual demand for conventional tablets is more than this of lyophilized products. So, you need to know what to expect in order to build the right business plan and strategy.

If as a CDMO you don’t do anything and just wait for a new trend to become mainstream, then you can reassure your boss that you do well in managing your risk but at the same time, you should manage expectations when it comes to growth and profitability discussion.

Being smart enough to invest at the right time in the right technology separates the best from the rest.

They Messed up and left…

A fictitious story about the mess that was created in a CDMO when an unrealistic business plan was asked to be delivered.

read the full set of articles here:

https://www.linkedin.com/newsletters/7001486756126576640/

Year end Thoughts About Strategy in the Pharmaceutical CDMO industry

The end of the year is the time to put your thoughts together, look back at what happened over the last 12 months and make plans for the ones that will follow.

So, I was thinking of the discussions we had with our partners all these previous months, their worries, their plans, and the challenges they faced in the pharma CDMO industry. Some of them were simple, some of them more complicated but all of them generated interesting discussions.

There were questions about the industry such as what will be the needs of pharma companies in the near future, who are really our competitors, what are other CDMOs doing better than us, is our level of cost within the market range? And then there were questions about internal challenges certain people at the top management faced, like what is the right profitability measurement that we need to use in order to capture more efficiently the impact of new business and discontinuations. Or discussions about the strategy to be followed and how realistic the targets are when it comes to business plan expectations, both in terms of timelines but also of figures.

Finally, there are those discussions we had with pharma companies, that face problems with their current CDMO, they want to understand if what they pay to CDMOs is fair or they have other concerns like for example wanting to add in their pipeline a new product and they can’t decide if they have to develop it from scratch or to in-licence it.

Playing all these discussions in my head, different thoughts come to my mind. I think for example how difficult is to convince internally that from now on, on top of gross profit we need to start also looking at contribution margin for new quotations and this is because our manufacturing site is not underutilised any more and fixed costs are already covered by existing products. So, we don’t need to cover every time all our fixed costs and add on top a margin, especially when the customer is not ready to pay this amount. It might sound easy, but I dare you to try make this discussion with the CFO of a CDMO, who has set the profitability target for new business at 30% and overall EBITDA level of 15%.

Similarly, presenting to the board the impact of discontinuation of a loss making product, it is much trickier than it sounds. If the product is discontinued, but the direct labour cost related to it remains, what is really the impact? And if fixed costs of the site do not go down, what will happen to the profitability of other products that will remain in site? Will they have to absorb more fixed cost from now on? And then what will be the impact on their profitability? To me these are very interesting discussions but rarely people have the time to dive deep into the figures and make this analysis. Let alone that starting such a discussion may trigger other discussions about cost cutting. And nobody wants to start talking about this. So, unfortunately the convenient way of approaching the matter is to continue doing things the way they used to be done up until now.

Another difficult subject is to convince a board which intends to sell the company in the next years, that the 5 years business plan that is about to be created cannot be super challenging and unrealistic. Although it is nice to show to potential investors that in 5 years time, a CDMO can double its EBITDA, it is something that not all CDMOs can succeed in. Especially if the pipeline of new business is poor and new business will come from quotations that will be submitted in the future. But then, which Commercial Director or even which CEO will argue with the board that what you ask is unrealistic? The reply will be, if you believe that you cannot do it, we will hire someone who can. And so, second thoughts come to people’s minds and they avoid opening this subject.

Then, discussions about what price to give for new quotations and the strategy behind the pricing policy are the ones that intrigue me the most. Because there will always be this person with influence somewhere in the organisation who wants to standardize things. So, when the target for new quotations is for example set at 100 and profitability at 30, who will convince him that for the specific product that is about to be quoted with very high material cost, profitability cannot be 30 but it might be 15? Because if we stick to 30 it will be like adding 30% mark up on materials and this is something that is not acceptable by the market? So, is it better for the site which asks for new business to lose this opportunity and wait for the next, or is it better to provide a price with 15% margin and maybe win the business? And who will be responsible for this decision? Will it be the Site Head, the Business Development Director or the CFO? All of them have different priorities. Site head wants to add new business in the site as long as it is profitable, the Business Development Director wants to bring the customer in so to open the door for other new business also maybe for other manufacturing sites of the CDMO, and the CFO wants at least 30% profitability. If there is no common understanding and dialogue between them, then the one which is impacted negatively it’s the CDMO itself.

On top of all these, discussions about the growth strategy of a CDMO are also always interesting. How can we attract more new business, should we invest in Contract Manufacturing activity or into our own business (for integrated CMOs), in which technology should we invest. What the competitive environment that we operate looks like, what we can do better than our competitors, which are our direct competitors? I remember that when Fuliginous Management Consulting created the European CDMO Mapping including companies offering CDMO services, the number of companies in this database impressed me a lot. More than 330 companies offer CMO services for finished dosage forms of small molecules in Europe. Not, 100, not 200 but more than 330. This means that CDMOs that want to outperform should start adding more value to their customers in order to have some luck to increase their pipeline. And then discussions with our partners on what we can do better, where we should invest, what are the needs of the pharma industry start to take place. One way is to invest in new technologies that other CDMOs do not offer. Another way is to start offering services that we currently do not offer, like strong development capabilities. Because many CMOs have a “D” in their name, making them a CDMO, but how many of them can really develop a product from scratch? The truth is that not so many can do so efficiently.

But apart from the discussions we had with CDMOs over the last year, we also had discussions with pharma companies cooperating with CDMOs. Their main concern was to understand if what they pay for their existing products to different CDMOs is fair or if they can find synergies by negotiating prices or moving products to other CDMOs. Moreover, there are many pharma companies which suspect that the number of CMOs that they cooperate with, is big for the number of products they have in their portfolio. What is really the market average of the number of products vs the number of suppliers that a pharma company cooperates with? In a study that Fuliginous Management Consulting performed, the ratio of products / manufacturer has an average of almost 2.5. This means that a company with 100 products in its portfolio, cooperates on average with 40 suppliers. This was also a figure that impressed me, when I first found out.

And then we had of course discussions with several pharma companies, that wanted to outsource their production and they were puzzled to find the appropriate CDMO able to deal with the peculiarities of the specific product and having a good strategic match with them. The most interesting case last year, was a discussion we had with someone of the top management of a big VET pharma company who had asked more than 50 CDMOs if they can produce its VET, high potent, lyophilized product to be marketed in USA and all he got was negative replies. It was rewarding (also mentally) for us to find a solution for him, from a CMO that he had never heard before based in USA.

Approaching the year end, looking back but also looking forward, all these thoughts make me feel lucky that I have the opportunity to take part in such interesting discussions and being part of the solution. Politics inside organizations will never stop to exist, there will be different departments with different agendas and priorities, there will second thoughts in certain people’s minds but at the end of the day, all of those people work for the benefit of the organization. So, discussions around topics like the above should be made and progress will come only if people get out of their comfort zones. Strategic decisions should be based on information and having the knowledge of what the market is doing is something that always helps.

Pricing high value API products in the pharma CDMO industry. Trickier than it sounds

What is the right price to quote in order to win the business but at the same time secure profitability and avoid future surprises for our CDMO business? This is a question that probably everyone that has to provide a price for a new RFQ (Request for Quotation) has to answer.

This is not an easy question to be answered and this is because there are many ways to approach the matter, as well as different considerations that need to be thought of. But when it comes to high value API products (or expensive materials in general) pricing decision becomes more and more tricky.

According to Fuliginous Management Consulting there are 3 elements to consider before you decide what is the right price for a specific product. To increase the probability of getting the business with the highest possible profitability, all three elements should be combined.

- Cost Plus (where a profit % is added to the cost)

- Market Minus (what is the customer willing to pay for the specific product)

- Competition (what other CDMOs offer for the same product or type of products)

The first one is the easiest to apply because the only thing that someone has to do is to add on the total cost of the product a predefined by the top management profit %. If for example the guidelines are to have profit of 30% for every new product, the pricing for the new product will be based on this.

But if the other two parameters are neglected then we might leave value on the table or our price might be too high and thus the probability of success will be low. So, define what the customer is willing to pay should somehow be estimated and there are different ways to do so. One way is to find the price of the product in the market of interest and calculate a profit for your customer which you think it will be satisfactory for them. Another way is to see what prices you have quoted in the past for similar products (API, technology, customer type etc) and have made it to production.

Coming to what competition is offering for similar products is very difficult to know and this is because you never know what strategy each CDMO applies. Consider that there are 2 CDMOs that compete for the same product in an RFQ process from a customer that is very promising and asks for a full cost price. The product is a 50 mg tablet and has a high API cost (lets assume 5000 euros per kg). This means that the cost of the API per tablet is 0.25 (250 per 1000’s tabs), while the remaining cost of the product is an average one (lets consider 20 euros per 1000’s tabs), similar to both CDMOs. Lets also consider that both CDMOs want to have 30% profit, but the difference between the two is that first CDMO applies a profit % on the total cost, while the second CDMO does not ask for profit from the API (he just adds some working capital cost and some production losses assumed combined at 10% of the API cost) and adds 30% profit on the remaining of the costs.

It is clear that the prices of the two CDMOs will be totally different. The price of the first CDMO will be 386 euros per 1000’s tabs while the price of the second CDMO will be around 306 per 1000’s tabs. If we assume that the annual volume is 10 million tablets the annual difference in the spend is 800K euros. If the annual volume is bigger, then the annual difference between the two CDMOs will be even greater.

Of course profitability of each CDMO will be very different. In the first case will be 30% (1.1 million euros per year for the 10 million tabs) and in the second case 12% (360K euros for the same annual volume).

If everything else is the same between the two CDMOs, the customer will most probably select the second one, since the price of the first CDMO is 26% more expensive. The customer might also form the impression that the first CDMO is an expensive one in general, and this impression could lead in excluding this CDMO from future quotations.

But now consider the following situation. Two years later, when the transfer is completed and the product is into production in the second CDMO, something goes wrong, and a batch fails and needs to be destroyed or recalled due to fault of the CDMO. I wouldn’t want to be in the shoes of the CFO asking for the impact on profitability. Assuming 4 batches per year to produce the full volume, the annual revenue of the CDMO will be around 3 million euros and annual profitability as seen above 360K euros. The cost of the API per year is 2.5 million euros and since 1 of the 4 annual batches needs to be destroyed, the CDMO will have to pay from its pocket 625K euros. (annual cost of the API dived by 4). This is the profitability of almost 2 years, meaning that the CDMO will have to produce the next two years with zero profit in order to pay for the damage.

If the same happened in the first CDMO, with annual profit from this business of 1.1 million euros, the damage would be of course smaller. (Profitability would be decreased of course but the product would still be profitable in annual terms).

This brings to the table a dilemma. Which is the best pricing decision to make when quoting for high value API products? The one of the first or the second CDMO? Of course, there will be those arguing that adding 30% profit to the total business makes sense but on the other hand if there is competition who does not apply profit on materials, probably, business like this will never be won in the first place.

Is there a magic solution? Can someone guarantee that a batch will never fail? Mitigating such risk is necessary and certain actions can be taken, like increasing the quality level, strictly monitoring of processes, insurance for the API, etc, but if you were on the shoes of these two CDMOs, what would you do? Aiming for the new business from the promising customer or aiming for the peace of mind but decreasing the probability of getting the business?

It might depend on how much each CDMO wants to win the business and tolerance towards risk each CDMO has. It might also depend on the confidence each CDMO has in itself or even the financial security of each CDMO. And it definitely depends on the CDMO’s strategy for growth going forward. Furthermore, if a CDMO is already familiar with the product and its difficulty to produce, this might also help them taking the right decision. Finally, of course, it is also a matter of profitability measurement. On one hand there are CDMOs who set targets on profitability for new business considering their full cost including API and on the other hand there are CDMOs that measure their profitability as contribution on conversion (meaning profit expressed as part of the direct labour cost, where materials don’t affect profitability) and there are others in the between that add profit on materials but not as much as they do on their conversion cost.

But there are CDMOs which might not even think of such dilemma when quoting. These might be the ones with products with low-cost materials in their existing portfolio which may have not encountered such dilemmas in the past. There are also pharma companies cooperating with CDMOs that might not understand why offers received from two CDMOs for the same product can be so different.

This article hopes to give some food for thought to different stakeholders. Operating in the CDMO industry is not always easy and if pharma companies cooperating with CDMOs put themselves in the shoes of the first, cooperation will be easier. The same is true the other way around, putting yourself in the shoes of pharma companies builds stronger partnerships.

Being transparent also helps. If I was in the position of the first CDMO in the above example, I wouldn’t just provide a high price letting the customer make its own assumptions behind the reason. I would explain the rationale behind the decision, and although this might not be enough to win the business, it might not close the door to the customer for future RFQs. Likewise, if I was the customer in the above example, I would provide feedback to the first CDMO for its price (by the way this in not always done by pharma companies towards CDMOs) opening the discussion, and this might change the impression about the general competitiveness of the specific CDMO.

One thing is certain. Quoting for a new RFQ with high API value in the CDMO industry is trickier than it sounds.

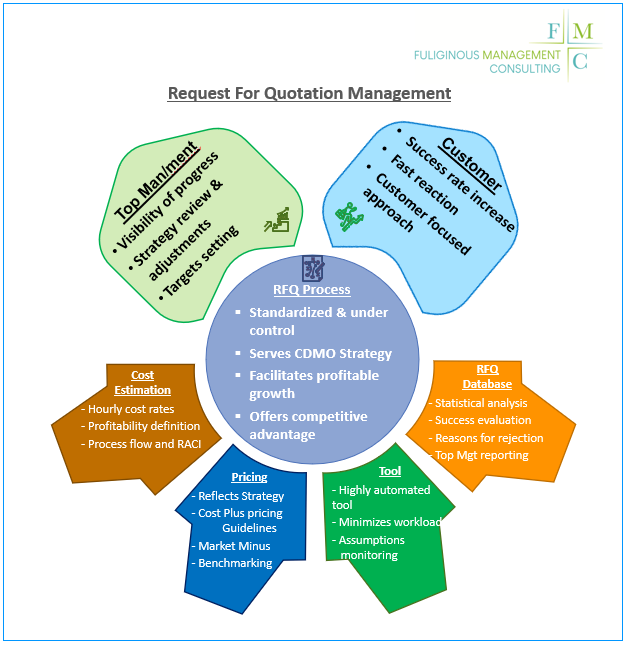

Request For Quotation Management: The oxygen generator for CDMOs

Contract Manufacturing (CM) continues growing globally at a CAGR between 6% and 8% as different studies and reports indicate. This is partly due to the increase in the global pharma business (mainly NPIs) and partly due to the outsourcing increase by the pharma companies.

On the other hand, the CDMOs’ established business is continuously confronted by challenges coming from products maturity (volume churn, market withdrawals), market specificities (price pressures, cost increase) and customer strategy (insourcing, supplier consolidation), leading to year-after-year top-line and profitability shrinking.

It is more than obvious that CDMOs, independently of the strategy they follow (“Growth” or “Stabilization”), are doomed to look for new business. New projects’ introduction is the oxygen they need, at least for keeping the CDMO in the business, let alone to support growth.

The fact that any new business opportunity passes first from the Request For Quotation (RFQ) process of the CDMO, makes the RFQ management the oxygen generation engine, the quality of which will determine the short and long term company health.

The result of the RFQ process builds perception and provides valuable information:

• Externally: Provides a strong indication to new but also to existing customers about the overall efficiency of the CDMO organization and the importance that the customer will receive from the CDMO.

• Internally: Secures future sustainability, provides valuable information for Pricing policy efficiency, expected future pipeline and facilitates realistic but challenging internal targets setting.

An efficient RFQ process has to:

• be standardized, fast and under control

• serve the CDMO strategy and facilitate profitable growth

• minimize offer preparation workload, facilitate project complexity management and monitor the process steps

• propose prices that increase probability of success and are within the desired/realistic profitability range

• provide competitive advantage and pass the right message to the customer

• facilitate statistical evaluation for strategic decision making

CDMOs (pure or integrated) have to make sure that the RFQ process gets the appropriate attention as it is one of the first cornerstones of their business and strategy sustainability.

The transformation journey of a manufacturing site from big pharma to a stand alone CDMO

There is a time in most peoples’ lives when they have to move from biking with support wheels to biking with 2 wheels. Apart from support, support wheels offer also stability, security and peace of mind. There is not much to worry about, you just have to move your legs and make sure you keep an eye on the road or the park. On top of this, usually a parent is with you to guide you and support you even more, whenever needed. When the time comes to get rid of the two additional wheels, a kind of transformation journey is required. You still continue to do the same thing (biking) but the challenges are many more. You need to adapt to the new reality, start focusing on different things, most important of which is to keep going since now you need to maintain a minimum velocity to stay upright. There is no support anymore when you turn, no guidelines from the parent when to break and this little rock or the sudden blow of wind can make you lose your balance. Let alone the fact that you gradually move away from the safe park and you start biking on the road.

To my eyes, the situation is similar when a pharma company decides to divest a manufacturing site and one fine day, instead of being part of a bigger family, the manufacturing site is left alone. Even if another CDMO acquires the site from the pharma company, it is often the case that it will remain independent with its own financial statements and resources. And although in such situations, during the first years of this transition, the site is protected (revenue protection, product volume protection etc.) this protection period is short. It can be three or four years, but this is not enough in the CDMO environment and the main reason is that in order to fill a site in three to four years you need to start preparing quotations now.

But it’s not only this. There are so many things that need to change in such situations. As it is the case when start biking alone on two wheels, a stand alone CDMO has no support or guidelines anymore from the parent company and no more secured business, and complexity increases dramatically. Instead of having to serve one customer, there is a need to start satisfying many more, instead of worrying about sticking to the production plan, attention to cost and profitability is required and among other things suddenly there is competition!

This means that there are many things that need to change in order to meet the new requirements and number one is the mentality. The mentality of the people working in the manufacturing site. And experience has shown that this is the biggest challenge of all.

Because it is difficult to change the mindset of people and explain that from now on they should be responsible for the profit and not just the cost, that OTIF should be at the same levels as this of the rest of the industry, that prices should be at the same levels as the rest of the industry and at the end of the day customers are those who pay their salaries and not the parent company anymore. From the moment that ownership changes hands, the people in the site need to start a journey; what I call a transformation journey.

But let’s deep into some details to understand the stages of this transformation journey. As mentioned above, one big change is that stand alone CDMOs need to bring in new business. And usually there is a reason that the pharma company decides to get rid of such manufacturing sites. It can just be due to a change in strategy, but it might well also be due to high cost, low utilization level, high investment requirements etc. So, if there is a manufacturing site with low utilization rate and with volume security (or revenue protection) for a predefined period of time, bringing in new business should be the number one priority. But its not only this. If costs are high and the new ownership wants to make profit, bringing in new business is not enough. You need to bring new business at the right price. The price that will allow good amount of new business to come in and at the same time to bring the desirable margin. And in order to do this, you need to know the market that you operate. You need to know what different customers are willing to pay for specific products and you also need to know what competition is offering.

On top of this, quality expectations should match those of your most demanding customer and delivery performance the same. As if this was not enough, as the years go by, the new owners will ask for growth. They will need to understand what is the cash flow, what is the expected profitability for the next 3-5 years, monitor the inventory levels, the working capital etc. They will even reach to a point where they will ask for cost savings! This does not necessarily mean layoffs, but it can mean that procurement department should make market research to find cost savings to raw and packaging materials, by negotiating with current suppliers or changing suppliers. The way of calculating the cost for new RFQs can be improved and the same goes for the pricing strategy and investment management.

Flexibility and customer service is another crucial area of attention. Form the very simple to the most complicated tasks. If competition provides a new quotation in two to three weeks, you cannot provide yours in a month. If a customer wants to split each batch to 5 different SKUs, you cannot afford to decline its request. When there is a failure in a batch and the customer is out of stock, you need to try your best to produce the batch again as soon as possible.

And then, there is contract management. As a stand alone CDMO, you need to make sure that your contracts protect and not harm you. You also need to be aware for contract clauses that enable you and for those that constrain you. And of course the entire organization should review a contract before it is signed and not just the legal team.

For all of the above to take place, new procedures and new tools will most probably be required. New KPIs, new monitoring systems and finally organizational changes cannot be avoided. There are dozens of new needs that have to be addressed and they need to be addressed fast, before existing volumes start moving out of the manufacturing site. And most importantly, all these changes need to be carried out without the support of a parent company. Just like starting biking with two wheels, except the transformation journey of a CDMO often proves to be a much more demanding challenge.

Private equity investment deals in the pharmaceutical CDMO industry. Separating the best from the rest. A fictitious story that teaches a lot.

Spring and summer is a great time to spend in Southern Europe, especially when all expenses are paid and you have given pocket money to spend. It was some years ago, when one family owned pharmaceutical CDMO, decided to change its ownership status from family to capital equity owned. And as it often happens, the private equity firm called the experts to have their say about the strategy to be followed and what should be expected.

The outcome of the first reviews and calculations was that this CDMO did not have a cost issue, it had a pricing issue. So, there was no need to visit the manufacturing sites, they would just take a look in the corporate functions and build the strategy. And specific attention should be paid to Business Development and Procurement departments. And this is what two well-known management consultants did. They spent their summer in Southern Europe and focused their attention to the corporate functions.

Long office hours, endless meetings, dozens of excel files, and the result was just great! A more than one hundred and thirty pages’ study and a more than one hundred pages new 5 years’ business plan were ready!

The Normalized cash EBITDA of the CDMO could fly from €10mio EBITDA, to €50-€60 million in just 5 years. The experts “sized a potential EBITDA upside of a great significance in 5 years from now”.

How? Very simple by approaching big pharma not yet in the CDMO’s portfolio, by finding additional opportunities among mid-sized pharma, by expanding in other geographies and technologies by saving in raw and packaging material cost due to higher annual volumes coming from new business, and the list goes on including other cost out initiatives of central management such as centralization of OPEX.

And of course, some prerequisites would support further the success story that was about to evolve in front of their eyes. A new pricing process, a new market intelligence team, new systems and tools, etc.

So, the solution was clear. Don’t change anything in the efficiency and the cost structure of the manufacturing sites, follow the above, and fasten your seat belt, you are ready for take-off!

So passengers sit, their seat backs and tray tables were placed in their full upright position and their seat belts were fastened. The flight attendances gave their guidelines for the take off and they… left the plane! The consultants were the first to leave.

The consultants left in the beginning of autumn and the same people in the middle management working only some months before for the family, were asked to begin transforming the company. The new owners, a big private equity venture, were happy and the journey began.

So, after the departure of consultants, people in the company started translating the business plan into actions. They started with the easy ones. And what is easier than kicking out some unprofitable business?

They started with a product which was well known of having negative EBITDA. And when someone from the top management raised the question how much is the positive impact that we have by discontinuing the specific unprofitable product, the answer was direct. “We earn the amount of EBITDA that we were losing before discontinuing it. So if we were losing €1 mio euros each year, the positive impact to the EBITDA is this amount”. Well… not exactly…

First of all, before answering this question, you need to understand in depth what does it mean “unprofitable product of €1 mio per year”

The second information you need to know to answer this question is what will happen to the costs associated with this product as soon as it is discontinued. Especially the fixed costs. Will they stay or they will be out too?

And this is where politics entered into the game. Business Development was arguing to operations that “I made what I had to make, I kicked out the product, now it’s your turn. Start cutting your costs linked with this product”. Operations did not want to cut their costs and finance was asking alignment between the functions for a common figure when it came to how much is the impact of the discontinuation.

Meanwhile the guidelines were clear. it’s OK to lose business, as long as they are not profitable.

To make the long story short, after two years, EBITDA was not increased and this was due to the fact that some business was discontinued, costs did not decrease and there was no time for new business to enter into the business. In the pharmaceutical CDMO industry, it takes time to quote, agree and transfer-in new business. And because of the new pricing policy dictating to quote with higher prices in order to improve profitability, it was getting more and more difficult to bring in new business.

And of course if two years from day 1 you are still on the same EBITDA level, with very limited new business agreements, there is no way to reach the 5 years target on time. As soon as it became clear to the top management and to the private equity investors that the target could not be met, pressure started to raise, the blame game began and of course the story could not have a happy ending. People in the top management, started one by one leaving the company and eventually the time came for the investors to start considering their exit with the minimum possible loss.

This was clearly an unsuccessful exit that was partly created by the unrealistic scenarios assumed in the first place. If the consultants that create the strategy do not have the expertise on the specific industry, and if the investors lack this expertise as well, it is easy to believe in something that an expert in the pharmaceutical CDMO industry could tell that is based on generalities and finally it is unrealistic.

It is no secret that private equity investors ideally look for high returns as soon as possible, but this has to be combined with the specific industry peculiarities. Of course there are opportunities for successful deals in the industry within 5 years window but specific market experience is required.

In order to create a successful exit strategy you need to have a realistic business case that convincingly answers the questions WHAT, HOW and BY WHEN and take actions that do not undermine the future of the company. In our case above, these questions were answered in an incomplete way.

- WHAT: the general directions provided by the Consultants were not broken down to details.

- HOW: not really touched upon.

- BY WHEN: CDMO market peculiarities had not been taken into consideration.

It is not realistic for example to assume that unprofitable business (that cover part of the fixed costs and overheads) will be discontinued and the financial picture will get better. If you remove the revenue and you keep the cost, the picture will be worse.

If you increase your overheads because you need to make a more professional business development and finance team, you need to consider that you cannot wait for improvements in EBITDA in the first years. On the contrary, profitability may go down before it goes up again due to some preparatory work that might be needed. And before you decide to increase your pricing levels for new business, you probably need first to take into consideration the market that you operate. If a CDMO manufactures conventional tablets (along with hundreds of other CDMOs in this world) increased prices will lead to lower success rate in the new quotations, meaning less new business for the same level of submitted offers. If the strategy involves increased prices to existing customers (without considering contract clauses in place) it should also assume that some of those customers will decide to leave. And if this happens, a cost adjustment should take place, not only in direct but also in fixed costs. (in order for EBITDA to remain untouched)

Creating a business plan that sounds attractive to investors is easy. The difficulty lies on creating a business plan (including an exit strategy) that is aggressive but also realistic both in terms of financial expectations and timing.

Before suggesting to invest in a new technology, you need first to understand the competition and the overall market of this technology. It easy to suggest investing in soft gelatin capsules or blow fill seal but the proposal should include what is the competition of the specific market, what are the difficulties in the manufacturing process, how many potential customers are out there and what are they ready to pay for these technologies.

Do they currently outsource their products to other CMOs, do they produce them inhouse or they have in-licensed the products and they keep the production to other pharma companies which out-licensed the dossiers to them?

Before suggesting increasing the price level or the profitability expectations, a strategy should consider what type of products the CDMO offers and what is the market average in terms of price level and profitability for these products and not just for the technology type i.e. tabs or amps. In general, before estimating the growth potential of a CDMO, deep knowledge of the industry is required.

And the same goes for cost reduction opportunities. Even if many times neglected, cost is one of the primary factors for near future business sustainability, especially in technologies with increased competition. It is common that CDMOs see their profitability decreasing year after year. The main reason for this is poor cost management and limited or no actions taken addressing cost increases. Identifying the cost level through benchmarking, determine the reasons for cost increases and suggest procedures and actions for efficient cost increase management is necessary. This will illustrate where room of improvement lies, what and how much benefit could be targeted and what expectations investors should have before proceeding with the deal.

And of course business development mentality is also core to achieve growth. Industry experts can tell if a specific business development team works according to best practices and what (and if) room for improvement is there. Current processes and way of working, understand how customer focused the Bus Dev team and the supporting organization is, RFQ management and lead identification processes are items that is difficult to be evaluated by investors without the support of industry experts.

Separating the best from the rest when it comes to business strategies creation that will be followed by private equity investors is straightforward as long as people involved in their creation know what to look for. Part of the job of those who consult private equities is to manage their expectations and explain to them the real picture in order to avoid future disappointment. You cannot expect from investors to know everything about the business, but you should expect it from the market experts.

Pricing in the Pharmaceutical CDMO environment

Market related factors include what competition offers for the same product but also what the customer (the pharmaceutical company which outsources) is willing to pay for the specific product. It is the combination of three elements that should, in my opinion, be considered when a CDMO offers a price. CDMO’s internal parameters, Competition and Customer’s willingness to pay.

CDMO’s internal parameters should not include only cost related factors. There is so much more than the cost that should be considered. It was some years ago when I was about to propose a price to a customer which asked for a price without API. It was a low annual volume product (couple of batches per year), difficult to produce and API would be provided by the customer free of charge. During a meeting where we would discuss what price to offer, the CCO asked the question. What is the Value of the API? Since the API price would be provided free of charge, nobody had bothered to evaluate what was its cost. But it turned out to be that this was a crucial point because the API value finally was double than the value of the remaining batch cost. What would happen if a batch failed due to CDMO’s fault? It was calculated that if the CDMO had to pay for the value of one rejected batch, this would mean that not only the profit of one year would be evaporated but also CDMO would run at a loss. It doesn’t matter what finally was decided in the specific example. It feels to me that this is a nice example explaining that cost should not be the only parameter that should be considered when a price is about to be offered to the customer.

But of course, there are more. Free available capacity, difficulty of manufacturing the product, complexity, expectations of more business from the specific customer are some of the internal parameters that should be considered. It maybe the case that the CDMO charges a premium for a product that is difficult to manufacture, especially if competitors cannot cope with it. Similarly, if free capacity is limited, maybe it makes sense to charge a premium for giving away this limited free capacity. On the contrary, if the specific project is a door opener for a new promising customer, then it might be wise to consider sacrificing part of the margin, in order to bring the customer in. This of course is related to the strategy of each CDMO. Some have a growth strategy, for some others next year’s EBITDA is more important.

It is not the scope of this article to go into details. It is to give some food for thought and therefore further elaboration of internal CDMO’s parameters will be avoided. And this gets us to Market related factors.

Since what price competition is offering for similar products is difficult to know, unless maybe you ask for external advice, lets jump to what the customer is willing to pay for the specific product. CDMOs should, in my opinion, put themselves in the shoes of their customers for a while.

Is the customer willing to pay more because the CDMO has limited free capacity? Does the customer care if the CDMO has a growth or an EBITDA related strategy? Probably not, but maybe a difficult manufacturing process plays a role in the price that pharmaceutical companies are willing to pay. Of course there are more important parameters that the latter consider when deciding on what is a fair price to pay. The most important of which is what margin this price (which is a cost for the customer) leaves them on the table. And this is where it starts to get difficult for the CDMO. Defining what is the margin of the customer, letting alone what margin is enough for their customers might be seen as a long shot. Nevertheless, there are some ways to approach it. And the closer they get, the better the chances are for defining the right price for the product.

Is it the same if a product is a commodity like generic paracetamol tablets as if the product is an innovative lyophilized vial, patent protected? Manufacturing technology, therapeutic area, competition in the market of the pharma company (how many other pharma companies market this product) and country of sale are some of the parameters that affect what is the willingness to pay.

A good approach for the CDMO to define the margin that its price will leave to its customer, is to see what is the price of the specific product in the pharmacies in different markets, remove taxes, pharmacy margins and distributor margins and get a flavor of the margin that its customer will have. Of course this is not enough. Different pharmaceutical companies have different expectations on their margins but in general there are specific patterns. For a commodity like a generic paracetamol tablet probably something around 60% is fair enough. On the other hand, for an innovative lyophilized patented vial, they would expect something around 90%. These figures exclude rebates and marketing costs that pharma companies need to pay. If the CDMO does not consider factors like this, providing a price only based on internal parameters significantly reduces the chances to provide the appropriate price. Although it is difficult for many CDMOs to run this exercise, it probably worth the time and the effort.

Yet, margin is not the only factor affecting what is the willingness of a pharma company to pay. Culture, location, quality, cooperation, responsiveness and flexibility of the CDMO also affect customers’ willingness to pay. If the pharmaceutical company is satisfied with the service level they get from a CDMO, if they feel that they are important and their supply is secured, they are probably ready to sacrifice part of their margin as opposed choosing a CDMO with a lower price but also a lower service level and higher supply risk.

And of course, the better the pharmaceutical companies outsourcing their products are informed about what is the average price in the CDMO market for the specific product, the more ready they are to answer what is the fair price to pay.

Most pharma companies know that persisting in receiving a very low price from a European CDMO only because they want to keep their margins at a certain level, will not work in the long run. If the average conversion price in the European CDMO market is 2 cents for a simple tablet, asking to receive it at 0.5 only because they want to keep their margin above 60%, is not realistic.

Even if there is a CDMO that will accept to provide such price, in the long run this cannot be viable. His costs will continue increasing year after year and one day he will ask to change the price to a level which will be closer to the market average. Or, worse, he will inform the pharma company that he cannot afford continue producing it anymore.

So, answering the question what is the right price to pay (or to charge) it needs market knowledge. Knowledge of the CDMO market but also knowledge of the pharmaceutical market. CDMOs should put themselves in their customers shoes but the opposite is also true in order to have a healthy long-standing cooperation.

Knowledge of the market is important. Get to know your market but also get to know your customer’s market. Combining both will make you better prepared to answer the question of what is the right price in the CDMO environment.

Designing a new business plan in the Pharma CDMO industry. Are you ready to wait?

So, next time you hear someone building an aggressive business plan in terms of timelines and growth in the pharma CDMO industry, ask for details and look for realistic explanation. Important rewards should be expected at least 5 years later. Let’s see why with an example.

First let’s set some basic assumptions. Usually periods following a crisis, change of ownership, or attempts to set an organization from scratch require a reset. This means that limited or no new business has been agreed at time zero. Therefore, all effort starts now. And effort begins by providing new quotations to customers, wait for their response, and ultimately agreeing some new business. Then, begin the technology transfer, succeed in validation batches, perform stability studies, register to health authorities the new manufacturing site, hoping that everything will go according to plan. Only then the CDMO is ready to start producing the commercial batches.

The below example uses the following basic assumptions:

Target for revenue coming from new business is set to 100. Let’s see by when this target can be reached taking the below assumptions:

- Each year the CDMO has the resources to submit quotations of 100 worth of revenue

- Success rate of submitted quotations to customers is set to 20%. This is the average of the CDMO business as experience has shown

- So, according to this success rate, each year the CDMO can agree 20 worth of revenue from new business

- Completion time of transfer: 18 months

- Revenue of new business agreed coming from routine productions will come gradually. In an optimistic scenario: 25% on the first year, 75% on the second year and only in the third year the full agreed revenue will be materialized. This is because in the first year, some limited revenue might be expected from validation activities, in the second year routine productions will not start in the beginning of the year, or not all SKUs will be produced (for a more complex project), and on the third year, assuming that all countries have been registered to health authorities and transfer is successful, full quoted revenue can be expected.

- For simplicity reasons, no discontinuation of existing products will occur as well as current portfolio will have no fluctuation in the foreseeable future.

The below table shows how agreed revenue from new business will be materialized through the years.

Due to the reasons described above, revenue will come gradually and as it shown by the table, total target of 100 cannot be expected to be achieved before year 6. Moreover, the total benefit from 5 years effort will come in year 7.