Surprise, Confusion, Frustration and maybe also a wry smile can be the outcome of comparing commercial offers for the same product, coming from different CMOs. Pharmaceutical companies looking to outsource their products usually run an RFQ containing a handful of CMOs, asking the latter to provide their offer for a specific product (or a basket of products).

It is not uncommon that the offers received have a big difference between them, when it comes to the unit price. And this creates puzzlement or even uncertainty to the pharma company comparing them. The usual excuses trying to explain the big range, can be that the batch size and the manufacturing location are different, or that different API suppliers have been used, or maybe different packaging material specifications have been assumed.

But what if all the above are the same and also Direct cost is the same between different CMOs? But still, the difference in the price is big? What on earth is going on? How two CMOs with the same Direct Cost can provide so different unit prices for the same product? So, why even if batch size, location, API suppliers and packaging specs are the same between two CMOs, their prices have so big gap between them? And if we assume that on top of those similarities, the two CMOs have the Direct Cost, this is certainly a reason to go nuts… Or maybe Not?

Let’s, dig beneath the surface a little bit. As I like to say, first things first. Price is different than Cost and although sometimes they are related, it happens very often that they are not. So, when the effort to explain the difference in prices between CMOs starts from the cost, this can lead to wrong expectations. There are more things that might explain the mystery, and in this article, we will try to shed some light on it. In doing so, we will use an example comparing two CMOs with the same Direct Cost asked to quote for the same product to the same customer.

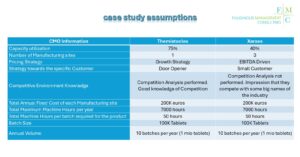

Let’s call the first CMO “Themistocles” and the second CMO “Xerxes”. And below is some information about them but also for the requirements of the product:

Assuming that both of them were asked by the same customer to provide an offer for the same product, the first thing they do is to calculate their direct cost. And then their fixed costs and overheads before deciding what price to offer.

Starting with Themistocles.

Direct cost for the product is already calculated and is assumed to be 15 euros per 1000’s tablets.

So, on top of it, fixed cost, overheads and margin should be added in order to calculate a price.

Fixed Cost Hourly Rate: Total Annual Fixed Costs / Total Annual Machine Hours x Capacity Utilization

So, for Themistocles this gives a fixed cost hourly rate of 38.1 Euros per Hour {200K / (7000* 75%)}. Considering a batch size of 100K tablets and that 50 machine hours per batch are required, the fixed cost is 19.05 per 1000 tablets. {38.1 x 50 hrs / 100K tablets)

Since Themistocles operates 1 manufacturing site, there are no corporate overheads to be allocated to the site. These costs usually have to do with corporate functions like corporate Finance, corporate Quality or corporate business Development and are common expenses serving as support functions for different manufacturing sites. Overhead Costs: 0 per 1000 tablets.

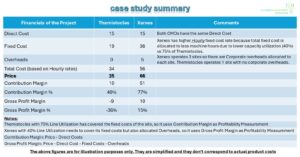

The business Case for Themistocles is as follows:

Direct Cost: 15

Fixed Cost: 19.05

Overheads: 0

Total Cost: 34.1

Since cost has been defined, now its time for adding a margin. Remember that Themistocles has 75% utilization rate meaning that probably fixed costs have already been absorbed from existing products on the site. 10 batches per year for the specific product, most probably will not require additional fixed costs (like a new Site Director, or New Supply chain Manager, additional rental, or additional utilities like heating for offices).

Therefore, Themistocles uses “Contribution Margin” to calculate its profitability. Contribution Margin is Price minus Direct Costs. Fixed costs and overheads are not considered in this profitability measurement. For as long as, the fixed costs do not go up if new products enter the site, contribution is the real profitability and what it goes directly to the bottom line of the site.

So, keeping in mind that the specific customer will work also as a door opener and Themistocles has a growth strategy, he is happy with a contribution margin at 40%. This will give a price of 25 euros per 1000 tablets and contribution margin of 10 euros per 1000 tablets. This price covers all direct cost and although (according to the hourly rates) does not cover fixed costs, this is not relevant for Themistocles since these costs have been already covered. In annual terms this project will result in 25K euros and 10K euros profitability. So the spent for the customer will be 25K euros if he selects Themistocles.

Lets do the calculations for Xerxes now.

Direct cost for the product is already calculated and is assumed to be 15 euros per 1000’s tablets.

So, on top of it, fixed cost, overheads and margin should be added in order to calculate a price.

Fixed Cost Hourly Rate: Total Annual Fixed Costs / Total Annual Machine Hours x Capacity Utilization

So, for Xerxes this gives a fixed cost hourly rate of 71.4 Euros per Hour {200K / (7000* 40%)}. Considering a batch size of 100K tablets and that 50 machine hours per batch are required, the fixed cost is 35.7 per 1000 tablets. {71.4 x 50 hrs / 100K tablets)

Remember that Xerxes operates 3 manufacturing sites and there are corporate overheads that need to be allocated in the sites. Let’s assume that the after doing the calculations, for the specific project the overhead cost per 1000 tablets is 5 euros.

The business Case for Xerxes is as follows:

Direct Cost: 15

Fixed Cost: 35.7

Overheads: 5

Remember that Xerxes has a low utilization rate and fixed costs have not yet been absorbed by the existing products. Moreover, the EBITDA related strategy means that every project should have a minimum profitability that should cover all costs and also leave a margin. This means that Xerxes cannot use contribution margin as a profitability measurement. Instead, he should use gross profit margin measurement. This measurement considers that all costs need to be removed from the price to determine what profitability the project will leave.

Moreover, this is a customer that for Xerxes is not considered important, meaning that he is not ready to sacrifice his profitability.

So, even with a gross profit of 15%, Xerxes would have to give a price of 65.75 per 1000 tablets and gross margin 9.86 per 1000 tablets. This price covers all direct and fixed costs and overheads and leaves some profitability on top. In annual terms this project will result in 65.7K euros and 9.9K euros profitability. So the spent for the customer will be 65.7K euros if he selects Xerxes.

This is a difference between the two CMOs of 40.75 per 1000 tablets or putting it in another way, Xerxes price is 2.6 times higher than Themistocles.

This might look like an extreme example but the truth is that experience has shown that such differences can occur in real life. In Fuliginous Management Consulting we have run RFQs on behalf of our customers where the lowest from the highest price coming from different CMOs can be 3 times away or even bigger.

And this is the top of the iceberg since we have not taken into account factors like batch size, machine output, manufacturing location which impacts direct labour cost, not even how different CMOs approach material costs. There are some CMOs for example who just add a small % on top of their material costs (to cover the working capital for example) while other CMOs apply the same profitability % as the one they use for the overall product. So if the latter want to have 15% gross profit, then they will apply this also on materials. If the materials is a big part of the price, then the difference with other CMOs can be significant.

And of course, this proves that a big number of CMOs do not spend time on understanding what the customer is willing to pay for the specific product. Putting yourself in the shoes of the customer is something that takes time but at the end of the day it improves the probability of success in RFQs.

Cost Plus Pricing Model alone is introvert and does not take into consideration the market peculiarities. Market Minus model (what the customer is willing to pay) and Benchmark of the competition (what other CMOs offer on average for similar technology products) should be in place if CMOs want to win as many RFQs as possible that are relevant to their strategy.

So next time you receive offers from different CMOs with a big range, there is no need for surprise, confusion or frustration. Its not that expensive CMOs want to “steal” you, they just have different pricing strategy, or they have not gone deep enough in their costing and profitability policies. It might be also the case that the CFO and the Commercial Director of the CMO have different views on how the ideal project looks like. And it might be also matter of timing. At different time points the same CMO may have different utilization rate, different equipment, or different profitability targets.

Trying to solve the mystery behind pricing requires deep knowledge of the pharma CMO industry, costing and pricing. But one thing is certain. By understanding factors that influence CMO pricing, Pharma companies can make more informed decisions and avoid unnecessary confusion or frustration when comparing offers.